The Gambling Review White Paper: Financial Risk Checks (AKA Affordability Checks) for Online Operators

![]() United Kingdom (May 30, 2023) — One of the issues which prompted the most debate in the lead up to the White Paper has been the notion of ‘affordability checks’ for online operators i.e. whether – and the extent to which – gambling companies should be required to satisfy themselves that their customers can afford to spend the amounts that they have lost or may lose in future and, in order to do so, requiring customers to provide financial information, such as bank statements, payslips, tax returns etc., to evidence their income.

United Kingdom (May 30, 2023) — One of the issues which prompted the most debate in the lead up to the White Paper has been the notion of ‘affordability checks’ for online operators i.e. whether – and the extent to which – gambling companies should be required to satisfy themselves that their customers can afford to spend the amounts that they have lost or may lose in future and, in order to do so, requiring customers to provide financial information, such as bank statements, payslips, tax returns etc., to evidence their income.

The speculation and uncertainty over where the Government would land on this issue was one of the biggest causes of concern for online operators arising from the Gambling Act review and raised serious doubts over the future and sustainability of the industry in Great Britain, particularly with some calling for these checks to be carried out if a customer spent more than £100 in a month.

The issue goes to the heart of the balance that Lucy Frazer described in her ministerial foreword to the White Paper between “consumer freedom and choice on the one hand, and protection from harm on the other”. Many ask why is it that financial checks are appropriate in the context of gambling, but not other forms of (potentially reckless or harmful) consumer spending, such as significant expenditure on holidays and luxury goods. In addition to the freedom of choice arguments, many companies have been concerned that the requirement to provide such personal financial information would either discourage customers from gambling altogether or push them to black market operators. Horseracing, in particular, has expressed concern that intrusive affordability checks could lead to a material reduction in the sport’s income from betting.

What was the requirement in terms of conducting affordability checks prior to the White Paper?

Although much of the debate has been about whether such affordability checks (renamed by the White Paper as “financial risk checks”) should be introduced, these checks have been encouraged (and increasingly required) by the Gambling Commission since 2019, when it amended LCCP Social Responsibility Code Provision (“SRCP”) 3.4.1 and implemented its formal Customer Interaction Guidance. The Commission has over time emphasised through its Enforcement Reports and enforcement action that it expects operators to assess affordability, including through requesting documentation and evidence from customers.

As the concern about the impact of affordability checks – and the campaign against them – grew, the Commission’s Chief Executive, Andrew Rhodes, said “there is a significant amount of misinformation circulating about the Gambling Commission’s position on issues like affordability”, noting that the Commission has “not imposed blanket so-called ‘affordability checks’ or set limits on what we think anyone should be ‘allowed’ to spend”. Whilst it is, strictly speaking, true that no blanket affordability checks have been “imposed” by the Commission, there can be little doubt that the Commission’s expectation is (or, at least, has been) that operators will apply them at relatively low levels of spend. The obligations under the LCCP are so broad and the guidance so high-level that operators sensibly fear that in light of the mood music from the Commission (and often having been subject to enforcement action by it), they are required to conduct arguably intrusive affordability checks at relatively low thresholds.

In the Annex to this article, we give a brief history of the Commission’s convoluted and tortuous position on affordability checks.

The detail of the proposals in the White Paper for affordability checks

The White Paper’s proposals in relation to affordability checks are set out under the heading “Account level protections” and state:

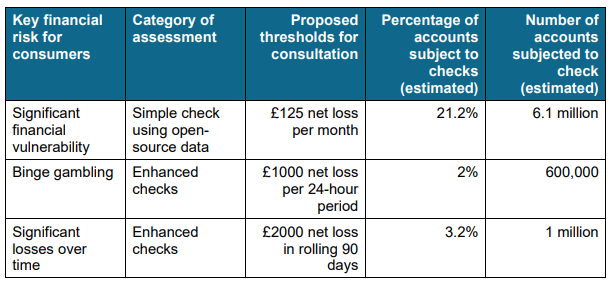

- The Commission will consult on new obligations on operators to conduct checks to understand if a customer’s gambling is likely to be harmful in the context of their financial circumstances. This will target three key risks identified by the Gambling Commission in its casework: binge gambling, significant unaffordable losses over time and financially vulnerable customers.

- In general, this Government agrees with the principle that people should be free to spend their money how they see fit, so we propose a targeted system of financial risk checks that is proportionate to the risk of harm occurring. Assessments should start with unintrusive checks at moderate levels of spend (£125 net loss within a month or £500 within a year), and if necessary escalate to checks which are more detailed but still frictionless at higher loss levels where the risks are greater (£1,000 loss within a day or £2,000 within 90 days). We also propose that the triggers for enhanced checks should be halved for those aged 18 to 24.

The White Paper also confirms that: “Neither the government nor the Gambling Commission will set universal rules on what proportion of a customer’s income they should be permitted to gamble, but the intention is that these checks should be used to detect and prevent harm alongside all the existing obligations to consider a range of indicators of harm”.

And, in more detail, the Commission is to launch a consultation on the following this summer:

i) Financial vulnerability

- At a moderate loss threshold (we propose either £125 net loss within a rolling month or £500 net loss within a rolling year), operators should conduct a financial vulnerability check, considering the types of open source indicators which many already routinely assess such as County Court Judgements, average postcode affluence, and declared bankruptcies. These checks should take seconds to process and would be frictionless for the consumer. We estimate that only around 20% of accounts in a calendar year will trigger this check as most never lose this much gambling. Net loss means the loss of deposited money with a particular operator, and does not include the loss of restaked winnings from that operator.

- If the check raises concerns and no robust evidence to the contrary can be provided, operators will need to respond accordingly. A range of actions may be appropriate, depending on the risks identified and the customer’s broader risk profile, and this will be considered further in the Commission’s forthcoming consultation.

ii) Binge gambling

- In line with the Commission’s advice, we propose that any account with net losses exceeding £1,000 in a rolling 24 hour period should be subject to an enhanced spending check which provides much greater insight into a customer’s financial situation by accessing more personalised data to consider factors like discretionary income. Such rapid losses are highly unusual and exceed the discretionary income nearly all people likely have available for a day’s activity, so are therefore highly indicative of risk.

- The Commission is currently working with the financial services sector to explore how more detailed checks could work in practice, and the expectation is that the majority would involve credit reference agencies and would not interrupt the customer journey unless the check raises concerns. We would expect the credit reference agency would be able to provide an overview of pertinent information for the individual customer, for instance an estimate of overall disposable income, rather than providing all the raw data to gambling firms. Where this is not possible, information may need to be collected directly from the customer, although there may be scope for streamlining this process using open banking (subject to safeguards to be explored through the Commission’s consultation). As now, this data will be used to inform an assessment of whether a customer’s level of spend is likely to be harmful to them. Again, a range of operator responses may be appropriate depending on findings and the wider risk profile, including applying limits to an account or ending the customer relationship completely where there are serious concerns. The details of the expectations on operators will be explored through the Commission’s forthcoming consultation.

iii) Sustained heavy losses over time

- Unusually high losses over a period of weeks or months are also sufficiently indicative of risk to be worthy of thorough investigation. In line with their advice to this Review, the Commission will consult on a proposed threshold of £2,000 net loss within a rolling 90 day period to trigger the enhanced checks outlined in section ii) above.

- Alongside assessing the risk of harm, these checks give an opportunity to fulfil operators’ wider ‘know your customer’ obligations, for instance by considering customers’ source of wealth and whether that presents any additional risks, for instance if it may be linked to money laundering or other crime.

- We additionally propose that Personal Management Licence (PML) holders should be more clearly accountable for ensuring that these checks are completed at the right time for all customers and that appropriate action is taken based on the findings. This is in line with the Commission’s efforts to increase PML holder responsibility for the businesses as a whole, and will be explored further by the Commission through consultation.

iv) Young adults

- A case was made through submissions to the call for evidence and in the Commission’s advice that those who are legally old enough to gamble but still relatively young (for instance those aged 18 to 24) may be at particular risk of gambling-related harm. The reasons for this include lower impulsivity control and other common life stage factors such as moving away from parents or managing money for the first time. Data shows that those aged 18 to 24 have the lowest average discretionary income of any adult age band and the lowest average gambling spend.

- Given these factors and the particular risks associated with remote gambling, we think there is a clear case for extra vigilance on the part of operators when a customer aged 18 to 24 spends an unusually large sum gambling online. We believe halving the investigation thresholds (i.e. to £500 net loss in 24 hours and £1,000 in 90 days for enhanced checks) is likely to be justified, and the Commission will explore this further through its forthcoming consultation.

In its advice to Government, the Gambling Commission summarises the proposed thresholds for consultations as well as the estimated number of accounts which would be affected by such checks:

So, where does that leave us?

Some operators will welcome the Government’s more prescriptive proposals for affordability checks in the context of the Commission’s ambiguous and apparently developing position, particularly given those proposals are far less stringent than some were campaigning for, both in terms of their thresholds and substance.

As can be seen from the White Paper’s language, the Government is keen to portray these “financial risk checks” as being as unintrusive as possible – hence, they will be “proportionate”, “unintrusive” and “frictionless”. It is expressly recognised that:

“In general, this government agrees with the principle that people should be free to spend their money how they see fit, so we propose a targeted system of financial risk checks that is proportionate to the risk of harm occurring.”

The Government does not appear to support the conduct of very intrusive checks, involving requests for documentation and evidence from the average customer. These are the sorts of checks that had become increasingly common under the Commission’s watch and the view in the White Paper appears to row back from that position somewhat.

In its advice to Government, the Commission refers to the checks at £125 net loss per month as “a light-touch assessment to identify particularly financially vulnerable customers”, whereas when referring to the checks at £1,000 and £2,000, the Commission says: “The aim is to reduce gambling harm by requiring operators to obtain sufficiently personalised financial risk information and to consider this data alongside other behavioural information. This will enable the operator to assess whether this level of loss indicates likely harm for the customer, and if so, take action which may include the setting of appropriate limits.”

The devil will be in the consultation though and some may be nervous that the consultation is to be carried out by the Commission (rather than DCMS) given the positions it has taken previously, in particular, in its Enforcement Report 2019 – 2020, that “[c]ustomers wishing to spend more than the national average should be asked to provide information to support a higher affordability trigger such as 3 months’ payslips, P60s, tax returns or bank statements”.

The Gambling Commission also now appears to give more weight to data protection concerns, such as the principle of data minimisation, than in previous years. In its advice to Government, it says: “A key principle of this work is data minimisation – identifying the minimum necessary data that must be collected from or shared about a small proportion of customers in order to meet the policy aims… We will continue to work with the Information Commissioner’s Office and the financial sector in considering these issues.”

It is also unclear whether the public is ready for or prepared to accept this degree of surveillance by the gambling industry simply to carry on with his or her gambling activity. One person’s “frictionless” check may be another’s invasion of privacy and unjustified intrusion into their freedom of choice. Such checks involve obtaining potentially highly sensitive personal data relating to customers and no doubt mistakes will be made. Customers have also expressed concern that unintrusive credit reference checks may nevertheless affect their credit rating when it comes, for example, to them making mortgage applications. On this point, the White Paper does say: “We will also make sure consumers’ financial lives are not impacted through these checks, with credit scores being unaffected and potentially adverse consequences of reciprocal data sharing avoided.”

The concern expressed by many (and particularly from those in horseracing) that excessive checks will either stop customers gambling or, more likely, drive many to unlicensed operators is addressed in the White Paper as follows:

“We recognise this risk, the chilling effect which asking customers for bank documents can have, and that implementing a financial risk-based approach will come with costs to operators. However, we think the impacts are likely to be mitigated by the proposals outlined above which mean no financial risk checks would be required for around three quarters of accounts, most of the checks will be frictionless with little interruption to the customer journey (for instance with credit reference or open banking data replacing the need for documents), and the provision of documents by the customer will be only a last resort for the highest spending minority. Further, it is our view that much of the foregone revenue is likely to be that which was coming from financially vulnerable customers or those who were gambling at significantly unaffordable levels, although this is hard to quantify”.

While the above proposals only apply to the remote sector, it is worth noting that the White Paper also says that: “[t]he current proposals apply only to the remote sector, but in due course we want to explore the use of frictionless financial risk checks where appropriate in land-based settings to benefit operators and help protect customers”.

In relation to unlicensed operators, the Government proposes the following:

“When Parliamentary time allows, we will introduce legislation that will give the Gambling Commission the power to apply to the court for an order that requires ISPs, payment providers and other providers of “ancillary services”’ to implement measures aimed at disrupting the business of an illegal gambling operator.”

The White Paper suggests that these powers will be similar to the “business disruption” measures proposed to be conferred on Ofcom as contained in the Online Safety Bill, which enable Ofcom to apply to court for a “service restriction” order allowing them to impose requirements on ancillary services (e.g. payment services) and, in certain circumstances, an “access restriction” order, which puts requirements on access facilities (e.g. app stores).

However, whereas “financial risk checks” can be implemented by the Commission under existing legislation, the Government’s proposals regarding unlicensed operators will require primary legislation.

It is not clear when the Commission will publish the results of its latest consultation on the new SRPC 3.4.3 and new Customer Interaction Guidance (which closed in January 2023) and, in particular, whether it will combine its further consultation on the three key financial risks with the consultation it will be conducting pursuant to the White Paper.

Annex – a history of the Commission’s approach to affordability checks

In 2019, the Commission amended LCCP Social Responsibility Code Provision (“SRCP”) 3.4.1 and implemented its formal Customer Interaction Guidance. SRCP 3.4.1 imposed a duty on operators to identify customers at risk of harm, interact with them and evaluate the impact and effectiveness of such interactions. It also required that operators take account of the Commission’s formal Customer Interaction Guidance, which required operators to take into account a range of account and play indicators, including those relating to spend, and expressly stated that “[m]ost people would consider it harmful if they were spending a significant amount of their discretionary income on gambling”.

This was followed shortly after by the publication of the Commission’s Enforcement Report of 2018 – 2019 which includes a section on affordability and refers to YouGov tables of monthly disposable income stating:

“For each age group, the data suggests that the GB population have disposable income per month from a figure of less than £125 up to £499. This is equivalent to less than £1,500 per year and £6,000 per year. However, even these disposable income figures do not take into consideration unavoidable monthly or annual costs such as transport, fuel, monthly contractual payments (mobile phones, cars, life insurance etc), vehicle maintenance, (service, repairs, and MOT), clothing and personal care. The disposable income data identifies clear benchmarks that should drive Social Responsibility (SR) triggers which will help to identify gambling-related harm by considering affordability. SR triggers should be set at a level so that most of the customer base is monitored based on the open source information.”

And, in the following year’s Enforcement Report 2019 – 2020, published in November 2020, the Commission stated that “[c]ustomers wishing to spend more than the national average should be asked to provide information to support a higher affordability trigger such as 3 months’ payslips, P60s, tax returns or bank statements”. The Report also gave examples where customers had been losing amounts which were clearly unaffordable and where operators had not taken sufficient steps to identify and protect the customers concerned.

Also that month, the Commission published its Remote Customer Interaction Consultation and Call for Evidence in which it said: “As part of these new requirements, we propose that online gambling operators must act on information they have about a consumer’s vulnerability, and to introduce stronger requirements, including that operators must conduct defined affordability assessments at thresholds set by the Commission. We are also calling for evidence on what the thresholds for these affordability assessments should be, the nature of these affordability assessments and how operators are required to protect consumers following an assessment. We recognise that there is a need to strike the right balance between allowing consumer freedom and ensuring that there are protections in place to prevent gambling that would have an adverse financial and health impact on consumers. It is necessary for an operator to understand whether a customer is gambling beyond their means to understand the risk of such harms”.

Following these publications and statements, as well as a series of significant fines imposed by the Commission, most operators understandably began to introduce forms of affordability checks for customers – though with the lack of any specific guidance as to when and how to conduct affordability checks, their timing and form have been left to operators to decide. The Commission’s approach has generally been that checks should be conducted earlier and earlier in the customer relationship and involve the provision of evidence of income by customers.

In November 2020, the Commission opened its Remote customer interaction – Consultation and Call for Evidence. This consultation resulted in a mixed reaction due to the Commission’s proposal to impose requirements to conduct affordability assessments at specific financial thresholds, with the lowest threshold at £100 loss in a month and the highest at £2,000 loss in a month. However, the Commission did acknowledge the need to ‘strike the right balance’ between consumer freedoms and ensuring that appropriate protections were in place to prevent gambling related harm.

The outcome of the consultation was, however, a long time coming – likely down to the fact that only a month later, in December 2020, the Government announced its review of the Gambling Act 2005. Many operators saw the Government review as an opportunity for clarity of the extent to which it was appropriate to curb consumer freedom through the conduct of affordability checks. Alongside that though, there was concern that the Commission would go ahead and impose affordability checks at specified thresholds without waiting for the Government to reach a view on policy, and on the balance between consumer freedom and the protection of vulnerable customers.

In September 2021, the Commission’s Executive Director, Tim Miller, said that revised LCCP remote customer interaction requirements would be published “in the coming weeks”. He stated “[j]ust to be clear, we are not talking about grey areas here. We are talking about significant binge gambling or clearly unaffordable levels of gambling without action being taken. Can anyone in this room seriously justify allowing a new customer to lose £10,000 within minutes without any checks or interaction?”. This was an apparent departure from the Commission’s position that affordability checks, involving requests for payslips or P60s, should be conducted before customers spend more than average discretionary income levels (as set out in its Enforcement Reports). He also confirmed the Commission would proceed with a consultation on thresholds for identifying key financial risks including significant losses in a short time, over a long time and financial vulnerability, but that it intended to wait for the Government’s review before consulting on issues covered by the review, such as being more prescriptive on affordability checks.

The Commission’s Remote Customer Interaction Consultation Response document, which included the new SRCP 3.4.3, was not published until April 2022. The Consultation Response document also confirmed that the Commission intended to conduct a further consultation “on the additional and specific steps operators must take to tackle three key risks with thresholds for assessment for each of these: (1) unaffordable binge gambling (2) significant unaffordable losses over time; and (3) failure to identify consumers who are particularly financially vulnerable”. We await this consultation. The new Customer Interaction Guidance to assist operators in complying with SRCP 3.4.3 was then published in June 2022.

It was initially intended that the new SRCP and new Guidance would come into effect in September 2022, but after feedback from the industry, the Commission postponed the introduction of parts of the new SRCP and the entirety of the new Guidance, which it said were to be the subject of a further consultation. The Commission’s previous Customer Interaction Guidance however ceased to have effect for remote operators in September 2022, meaning there is currently no customer interaction guidance technically in effect for remote operators (though it would be prudent for operators to have regard to both the existing and draft guidance in the interim period). The additional consultation was conducted towards the end of 2022 into early 2023, and requirement 10 of the new SRCP (relating to the prevention of marketing and the take up of new bonus offers for strong indicators of harm) automatically came into effect in February 2023. However, it remains unclear when the outcomes of the consultation will be published and when the remainder of the new SRCP and Guidance will come into effect.

The new SRCP requirements (to the extent they are in effect) are considered to clarify the Commission’s expectations as regards customer interaction and build on the existing LCCP and Guidance, elevating aspects of guidance to licence conditions and strengthening requirements in certain areas. In particular, the new SRCP requires the identification and specific action in respect of “strong indicators of harm”. The new requirements refer to customer interaction and the need to use a range of indicators to identify potential harm, including customer spend and patterns of spend (in a similar way to the previous Customer Interaction Guidance), but do not stipulate requirements as to the timing and substance of affordability checks.

By: David Zeffman, Anna Soilleux-Mills, Dan Tench, Tamsin Blow, Alasdair Lamb and Emily Sheard

SOURCES: CMS Cameron McKenna Nabarro Olswang LLP / Lexology.

Tags: money laundering, White Paper, Financial, United Kingdom, Internet & Social Media, Grambling